My big question is: Will there be an economic slowdown in 2020? The majority of economic experts say yes, while the political / economic pundits claim otherwise.

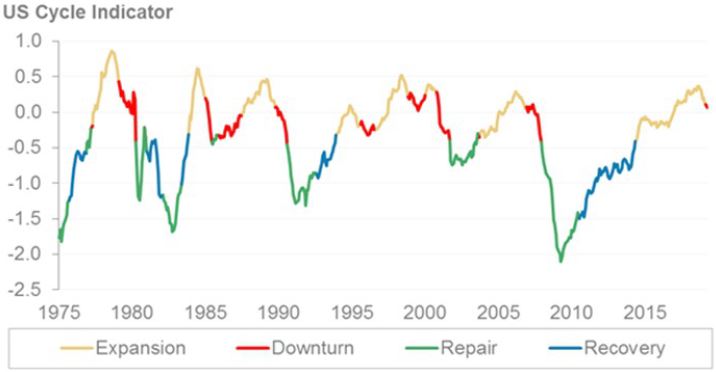

I’m of the school that there’ll be at least a significant economic slowdown in 2020. My thinking is based on fact that the US economy is cyclical. The current US economy has already surpassed the US longest economic expansionist period of 10 years (1991-2001); and the “inverted yield curve,” the most accurate past indicator of an economic slowdown within 2 years, has occurred in several months in 2019, starting in December 2018.

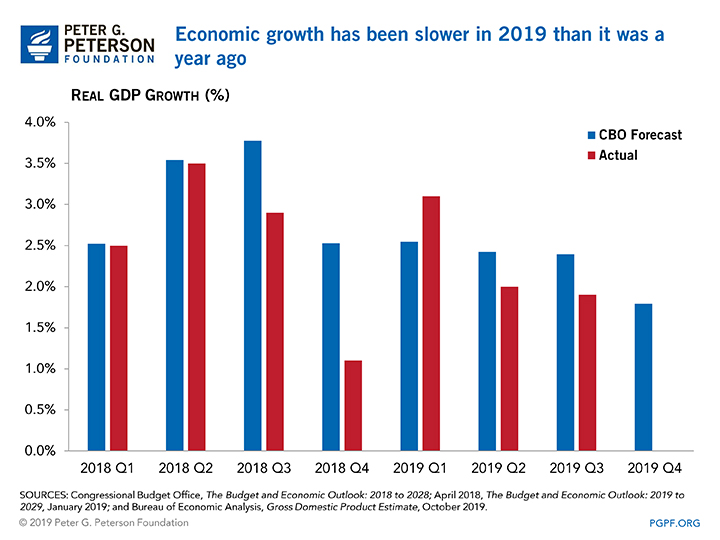

Other signs include the reality that manufacturing orders in 2019 have declined, consumer confidence numbers are on a downward trajectory; and the 2019 US economic growth for the 3rd quarter has slowed to 1.9%, a far cry from the 3% plus growth figures promised by GOP with the 2017 tax cuts.

It’s my opinion that the US trade war with China is a continuing drag on US economic growth and I’ve become convinced that there’ll be no real trade deal with specifics and of any consequence between China and US before the 2020 presidential elections. Fortunately, it appears that President Trump has successfully been influenced to not raise the subject of tariffs before the November 2020 presidential elections’ season.

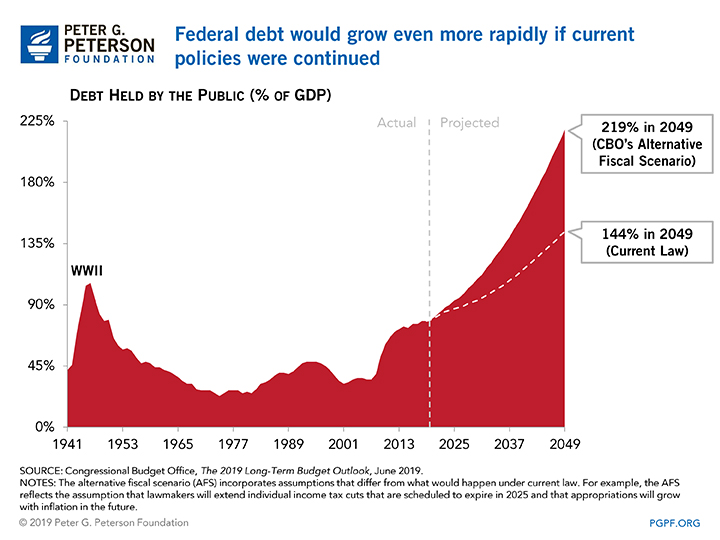

But the current US economy can’t continued to be propped up by being over $1 trillion dollars in debt forever. Most of us could live quite well with a trillion dollar credit card with no real plan to bring down this debt/ US deficit.

As per a 4/9/2018 CNN report by Heather Long, ” The federal government is on track to have a $1 trillion deficit in 2020 — and to continue running yawning deficits for years to come, the nonpartisan Congressional Budget Office predicts.

Basic facts:

As per the April 12, 2018 MoneyWeek report, “An inverted yield curve is what you get when the yield curve slopes downwards. In other words, investors are asking for more interest on short-term loans than on long-term ones.”

“It usually only happens when investors expect a recession and are therefore clamouring for the perceived safety of US government bonds.”

“In fact, “every US recession in the past 60 years was preceded by… an inverted yield curve,” note Michael D Bauer and Thomas M Mertens of the Federal Reserve Bank of San Francisco in a paper on the topic.”

Click here for a QuickTake on the yield curve

Here’s the rest of the story…

As per the October 30, 2019 Business Insider report, “The US economy slowed less than expected in the 3rd quarter amid strong consumer spending” Gina Heeb:

Excerpts:

- Economic activity cooled further in the third quarter amid ongoing trade disputes.

- Still, the 1.9% growth exceeded consensus analyst forecasts for 1.6%.

- The results cast further doubt on the prospect that Trump would fulfill his longstanding pledge to bring US growth to or above 3% this year.

“The record-long US expansion cooled further in the third quarter but kept up at a solid pace, as strong consumer activity partially offset the effects of ongoing trade disputes among the largest economies.”

“The Commerce Department estimated that gross domestic product, a broad measure of all the goods and services produced in a country, rose by 1.9% from July to September. Economists had expected 1.5% growth. In the previous quarter, GDP came in at 2%.”

“The data continues to show signs of a bifurcated economy,” said Michael Reynolds, the investment strategy officer at Glenmede. “The strong US consumer has continued to take the lead in driving this record-long domestic expansion forward, more than offsetting the headwinds from a slower manufacturing economy.”

“Consumer spending, accounts for more than two-thirds of activity in the economy, held up at a strong 2.9%. Households have remained one of the brightest spots in an economy faced with a flurry of strains, including steep tariffs on an increasing number of products.”

“While the US and China stalled further trade escalations this month, companies have continued to pull back on investment as they struggle with an uncertain outlook. Businesses spent less on capital this summer, with nonresidential fixed investment falling by 3%.”

“If businesses believe consumer spending is slowing they may slow their investments in plant and equipment, and eventually people,” said Gregory Leo, the chief investment officer at IDB Bank in New York. “It could become a downward spiral and lead to a recession.”

“The third-quarter GDP reading, which was the second lowest of the Trump presidency, cast doubt on the prospect that the White House would fulfill its longstanding pledge to bring growth to or above 3% this year. ”

“Even after a key recession warning flashed in August (inverted yield curve) for the first time since the global financial crisis, the Trump administration has continued to take a far rosier stance on the economy than independent forecasters and the Federal Reserve.”

“Policymakers on the Federal Open Market Committee have signaled they could lower interest rates for the third time since the financial crisis, a move that would bring the benchmark range to between 1.5% and 1.75%. A key measure of inflation, the price index for personal consumption expenditure, rose by 1.5% from July to September.”

As per a July 2019 Plant Engineering.com report, “Manufacturing technology orders down by double digits in 2019″ (“The Association For Manufacturing Technology (AMT) reported a 12% decline in manufacturing technology through July 2019 compared to the same period in 2018.”)

“U.S. manufacturing technology orders totaled $383.7 million in July 2019, an increase of 7% over June 2019 but a fall of 5% from July 2018, according to the U.S. Manufacturing Technology Orders Report published by The AMT. The total value of manufacturing technology ordered through July 2019 was $2.64 billion, a decrease of 12% from the 2018 year-to-date total of $2.98 billion.”

We suspect the impetus is the uncertainty with the current market and future economic conditions.”

“Machine shops decreased orders over the previous month for the first time since April 2019. The government and defense sector led all other industries in month-over-month gains but only accounted for a small fraction of the total orders placed. The automotive sector increased orders by more than half, and orders from aerospace increased a fifth from June 2019.”

“The North Central – East region led in month-over-month growth, where orders increased nearly 30%, while the region with the largest total decline SE. The West and North Central – West also saw gains over June 2019. The Northeast saw a very modest 1 percent decline, and the South Central narrowly avoided a double-digit decline, at 9 percent.”

“Other indicators show contraction, as well. The August 2019 ISM Manufacturing Report On Business reported the Purchasing Managers’ Index fell 2.1% points to 49.1. This is the first time in nearly three years the index has fallen below 50, signaling contraction in the manufacturing space.”

“Despite increased orders coming from the automotive sector, July lightweight vehicle sales fell or the second straight month to 16.8 million units on an annualized basis. Capacity utilization fell in July to 75.9%, the lowest reading since September 2017.”

“The University of Michigan Index of Consumer Sentiment fell to 89.8 in August, with a third of consumers making a negative mention of tariffs without prompt. The 8.6 point decrease over July 2019 is the largest monthly decline in consumer sentiment since December 2012.”

See report by (AMT) www.amtonline.org

As per the 9/24/2019 Bloomberg report, “Consumer Confidence in U.S. Declines by Most in Nine Months” by William Edwards:

Excerpts:

“U.S. consumer confidence posted the biggest drop since the start of the year as Americans’ expectations for the economy and the job market deteriorated, posing a risk to the household spending that is underpinning growth.”

“The Conference Board’s index decreased in September to a three-month low of 125.1 from a downwardly revised 134.2 a month earlier, according to data from the NY-based group. The median forecast in a Bloomberg survey of economists called for 133. Both the present situation and expectations gauges declined, with the latter dropping to the lowest level since January.”

- “U.S. stocks pared gains and Treasury yields fell after the report. Trade-war concerns and the economic impact are filtering through to Americans’ sentiment (while) businesses contend with fragile global growth and supply-chain challenges tied to uncertainty over tariffs.”

- “The overall measure remains elevated and within the range of the past year, suggesting consumers will continue to support the record-long U.S. expansion, though spending may moderate.”

- “The share of respondents who say jobs are currently plentiful dropped to a three-month low.”

- “Before the latest number, the Conference Board’s measure had been at odds with the University of Michigan’s index of sentiment, which has deteriorated since July. Economists at Deutsche Bank Securities posit that the gap widens ahead of recessions because the former is more backward-looking with its focus on employment, while the Michigan gauge is slightly more forward-looking because of its emphasis on personal finances.”

This blog was last updated on 1/28/2010.

It’s ironic that in blue collar places that support Trump most fervently in the South and Midwest are the ones being most in danger of being adversely affected by the upcoming economic slowdown.

LikeLiked by 1 person